Last Updated December 15, 2025 • By Zac Wasserman, REALTOR®

2026 Southern California Housing Market Forecast: Ventura County + Los Angeles Rates, Prices & Strategy

Looking for the 2026 Southern California housing market forecast?

This guide covers Ventura County and Los Angeles market predictions—mortgage rates, home prices, inventory trends, and practical strategies for buyers and sellers.

Understanding Ventura County real estate micro-markets

and Los Angeles County real estate micro-markets is essential for success.

What to expect in 2026: most major forecasts point to mortgage rates staying around the low-to-mid 6% range, with modest price growth and a slow-but-steady thaw in activity—more navigable, not a dramatic “boom.”

Published by Zac Wasserman (CA DRE# 02210760) • Local market insight for Ventura County + Los Angeles

2026 Southern California Housing Market Snapshot (Ventura County + LA):

• Rates: likely hover around ~6% to low-6% range (not back to 3%).

• Prices: expected to move modestly overall—local neighborhoods will vary widely.

• Inventory: improving slowly, but still tight in the most desirable pockets.

• Best opportunity: buyers who can act decisively; sellers who price correctly from day one.

Note: This post blends statewide/national forecasts with the most recent monthly local trend data available as of publication.

Rates

Likely “stuck” near 6%

Multiple 2026 outlooks point to elevated rates versus pre-2022 norms, with gradual easing rather than a cliff-drop.

Prices

Modest growth baseline

Forecasts generally call for modest appreciation nationally, with California behaving differently by submarket and supply.

Strategy

Preparation beats prediction

In a steady-rate environment, winning comes down to financing readiness, neighborhood selection, and realistic pricing.

Mortgage rates in 2026: what the forecasts suggest

The most consistent theme across major forecasts is this: mortgage rates may ease somewhat, but they’re expected to remain elevated compared to the 2010s and the pandemic-era lows.

For buyers preparing to enter the market, understanding how to get pre-approved for a mortgage in 2026 is a critical first step.

Realtor.com® projects mortgage rates averaging around the mid-6% range in 2026.

Reuters’ poll of property experts projected an average rate a little above 6% in 2026.

California Association of REALTORS® (C.A.R.) forecasted 30-year fixed rates around 6% for 2026 in its statewide outlook.

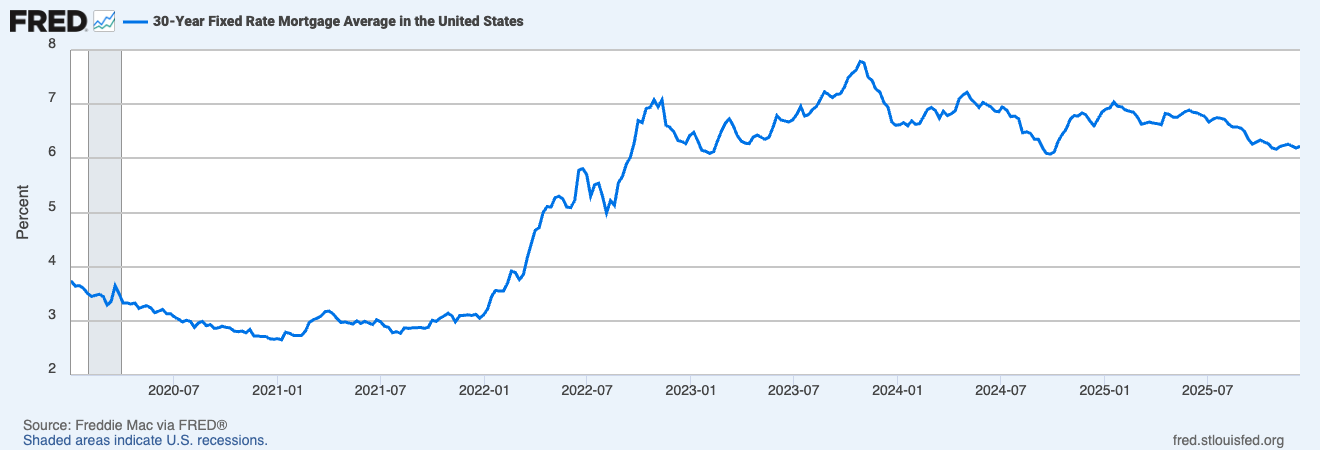

Here’s the good news for 2026 homebuyers: after three years of elevated rates, we’re finally seeing meaningful relief.

This chart shows the mortgage rate journey from the pandemic lows through today’s market—and the context you need for 2026:

Mortgage rates peaked at 7.8% in October 2023 and declined to approximately 6.2% by December 2025.

The trend shows rates stabilizing in the low-to-mid 6% range, with forecasts suggesting rates may remain near these levels through 2026.

Source: Federal Reserve Economic Data (FRED), Federal Reserve Bank of St. Louis

📊 What This Means for Your 2026 Home Plans:

Historic context: Today’s ~6% rates are far above 2020–2021 lows, but down meaningfully from the 2023 peak—and within the band many buyers can plan around.

The payment impact: A buyer financing $680,000 at 6.2% pays roughly $4,175/month in principal and interest. At 7%, that jumps to about $4,522 (roughly +$347/month).

2026 outlook: Most forecasts point to rates staying in the low-to-mid 6% range rather than dropping dramatically. That means focusing on payment comfort and neighborhood value—not timing the “rate bottom.”

The opportunity: Buyers have more time to evaluate properties, and sellers need to compete on price and condition—not just list and wait.

When it comes to the Southern California housing market in 2026, the consensus among analysts leans toward modest appreciation rather than surging growth.

The practical takeaway: your neighborhood matters more than the headline. Turnkey homes, strong school boundaries, and low-risk locations can keep pricing power even when the broader market is slower.

While appreciation will be modest compared to 2020–2021, both Ventura County and Los Angeles County show continued growth.

Here’s what the data suggests for median home prices through 2026:

Southern California Home Prices: 2026 Forecast

Median home price trends & projections for Ventura County and Los Angeles County

Why This Matters

Both markets show continued appreciation despite higher rates. Ventura remains more affordable than LA,

but both are seeing modest, sustainable growth—not the double-digit spikes of 2020–2021.

VENTURA COUNTY

2026: $870K–$895K

+1.5% to +4.5%

From 2025’s $857K

LOS ANGELES COUNTY

2026: $1.02M–$1.06M

+2% to +6%

From 2025’s $1.0M

💰 What These Prices Mean for Your 2026 Strategy:

Ventura County advantage: With medians ~$150K–$200K lower than LA, Ventura can offer stronger affordability for many families—especially in city-level price bands that still support conventional financing.

LA’s premium markets: At $1.0M+ median, LA remains price-stratified. Coastal and Westside submarkets often command durable premiums while affordability-sensitive areas react faster to rate changes.

The 2026 reality: Modest appreciation means sellers won’t get rewarded for “testing” a high price—execution, condition, and launch strategy matter.

Investment perspective: Sustainable appreciation plus principal paydown can still build wealth—just at a more durable pace than pandemic-era gains.

Ventura County baseline right now (latest monthly data)

Before forecasting 2026, it helps to anchor where we are today. The following Ventura County baseline metrics reflect the most recent monthly snapshot available at the time of writing.

Metric

Ventura County (latest month)

What it means heading into 2026

Median sale price

About $857K (latest monthly snapshot)

Pricing power is neighborhood-specific; “median” hides big swings by city and condition.

For city-specific insights, explore our guides to

Thousand Oaks,

Camarillo, and

Simi Valley.

Days on market

About ~60 days

Buyers have more breathing room than peak frenzy years; sellers must earn attention with price + presentation.

Sales volume

Roughly flat-to-up year over year (monthly)

Small improvements are possible if rates stabilize and inventory improves, particularly in “A” school boundaries and turnkey condition.

Data note: Use this as directional context. City-level and neighborhood-level conditions can diverge materially by street, school boundary, home condition, lot size, and micro-location.

Los Angeles baseline right now (latest monthly data)

The Los Angeles market in 2026 has a different dynamic: stronger price stratification, more investor activity in certain submarkets, and higher sensitivity to affordability.

Here’s the latest baseline snapshot at the time of publishing:

Metric

Los Angeles (latest month)

What it means heading into 2026

Median sale price

About ~$1.0M (latest monthly snapshot)

Affordability is the main governor; small rate changes can shift demand, especially for payment-sensitive buyers.

Days on market

About ~60 days

Condition and pricing discipline matter—buyers will pass on “almost right.”

Market behavior

Highly neighborhood-dependent

Expect “micro-markets”: one ZIP is hot, the next is flat, and the difference is often school + commute + condition.

Properties in Santa Monica, Manhattan Beach, Venice, and Malibu often maintain pricing power despite higher rates.

These markets have historically shown resilience during rate volatility due to limited inventory and high-income buyer pools.

Expect medians to hold or grow modestly (often 1–3%), with the luxury segment ($3M+) showing more volatility by property type and motivation.

Valley-floor markets (Ventura County)

Cities like

Camarillo,

Oxnard, and

Simi Valley

offer more affordability entry points for first-time buyers and families. These markets may see 2–4% appreciation as buyers priced out of LA expand their search radius.

Watch for increased competition in the $650K–$850K band where monthly payment thresholds cluster.

Hillside & view properties

Homes with wildfire exposure or insurance complexity may face headwinds. Buyers increasingly factor insurance costs into affordability calculations before writing offers.

For strategies on navigating these markets, see our

LA wildfire insurance guide

and

Ventura County wildfire insurance guide.

Commuter markets (LA County)

Areas like Pasadena, Burbank, and Glendale that balance LA employment access with strong amenities may remain firm if inventory stays constrained.

These markets appeal to buyers seeking strong “daily life” value without coastal premiums. Expect 3–5% appreciation where turn-key supply is limited.

If you’re buying in 2026: the smartest strategy

In a world where rates hover around ~6%, buyers win by being more prepared than the competition—not by waiting for a perfect headline.

Start by getting pre-approved with competitive lenders so you understand your real buying power and your comfort-zone payment.

1) Buy the payment, not the rate

Rates may not collapse. Your advantage comes from reducing payment volatility: stronger down payment, lender credits where available, and realistic price targets.

If rates do drop later, refinancing becomes an option—but it shouldn’t be your entire plan.

Calculate Your 2026 Payment

See how different rates and down payments affect your monthly mortgage payment

Your Monthly Payment (P&I)

This calculator shows principal and interest only. Your total monthly payment will also include property taxes, homeowners insurance, and HOA fees if applicable.

💡 2026 Payment Strategy Tip:

When comparing homes, calculate the payment difference between properties—not just the price difference.

A $50K cheaper home with higher taxes and insurance might cost more monthly than a pricier home in a better location.

Location drives long-term costs through property taxes, insurance, and resale value.

2) Target “A locations” and be flexible on the house

In mixed markets, location premiums usually hold. If you have to compromise, compromise on cosmetics—not the street, school boundary, or long-term desirability.

Research Ventura County school districts and

neighborhood quality indicators before making offers.

3) Use a two-track search: turnkey + value-add

Turnkey homes can still attract competition. Value-add properties can be less crowded—if you budget correctly and do your due diligence.

Strong listing presentation can also shape buyer perception; understanding fundamentals like

real estate photography

helps you separate “staged glow” from actual condition.

4) Build a fast but safe offer system

In 2026, the best buyers move quickly and protect themselves. Set offer ranges, define non-negotiables (insurance, HOA, condition),

and review our offer strategy checklist before you’re in a deadline situation.

A tight offer process often beats a slightly higher price because it reduces friction and uncertainty for sellers.

5) Don’t skip insurance diligence

In parts of Southern California, insurance availability and cost can affect affordability and even deal viability.

For insurance planning, use our pre-purchase insurance checklist.

If you haven’t read them yet, here are two related guides:

If you’re selling in 2026: how to win without guessing

If 2026 is “steady” rather than “explosive,” sellers need to lean into fundamentals: price it right, present it right, and market it like it’s competing (because it is).

1) Price based on today’s buyer pool

A buyer at ~6% financing is payment-sensitive. Overpricing can cost you the first 14–21 days, which is typically when your listing gets peak attention.

Use our seller resources including a home value estimator as a starting point, then validate with a full comparative market analysis (CMA) and on-market competition.

2) Condition matters more when buyers have options

Small improvements (paint, lighting, curb appeal, staging) can widen your buyer pool—and in a slower market, that is leverage.

Consider professional home staging to maximize first impressions and photo-to-showing conversion.

3) Use concessions strategically (not emotionally)

The best concessions are the ones that expand affordability: temporary buydowns, closing cost credits, or repairs that remove deal friction.

The goal is to increase the number of qualified buyers who can comfortably say yes—not to “negotiate against yourself.”

4) Treat launch week like a campaign

In 2026, execution matters. That means strong photos, clean disclosures, showing strategy, and pricing discipline—all aligned in the first week.

A well-coordinated launch reduces the chance your listing “goes stale,” which can force price reductions later.

💡 2026 Seller Timing Tip:

The strongest buyer activity typically occurs in spring (March–May) and early fall (September–October).

If your home needs work, start improvements in winter so you can launch when buyer traffic peaks.

A well-timed listing with proper preparation can command 3–7% more than the same home listed hastily in a slower month.

Local seller advantage:

If you want top-dollar, the fastest path is often: (1) accurate pricing, (2) clean presentation, (3) a strong first-week launch.

I can share comps + a launch plan for your specific neighborhood.

The 3 risks that could change the 2026 outlook

Rates move unexpectedly: inflation, bond market shifts, or economic shocks can change the cost of money quickly.

Inventory changes faster than expected: more sellers listing could soften prices; fewer could keep them firm.

Insurance/ownership costs rise: premiums, taxes, and HOA costs can change affordability even if rates don’t.

What changed from 2025 to 2026: market evolution

Understanding what shifted between 2025 and 2026 helps explain current market dynamics.

For historical context, review our market analysis archives.

Mortgage rate stabilization

After peaking above 7.5% in 2023 and hovering in the high-6% to low-7% range through much of 2024–2025,

rates stabilized into the low-to-mid 6% range by late 2025. That stability reduced payment shock and brought more buyers off the sidelines—not a flood, but a steady thaw.

Inventory gradually improving

After years of tight supply, more homeowners listed as they adjusted to the reality that 3% rates may not return soon.

This created a more balanced environment where buyers have choices and sellers must compete on price and condition.

Insurance becoming a deal factor

What used to be a closing-week detail is now a pre-offer consideration in many hillside and high-risk zones.

Buyers increasingly request insurance quotes before writing offers, and sellers proactively share policy details to reduce deal friction.

Payment-driven decision making

Unlike the 2020–2021 frenzy, 2026 buyers lead with monthly comfort. That creates price ceilings in certain submarkets and forces sellers to align with today’s qualified buyer pool.

Most major forecasts expect rates to hover around the low-to-mid 6% range in 2026, with uncertainty by quarter and market conditions.

The most practical approach is to plan for a payment that works at today’s rates and stay flexible if refinance opportunities appear later.

Key insight: Even if rates drop to 5.5% later in 2026, the payment difference on a $680,000 loan is often only around $200/month—meaningful, but not always worth delaying a purchase if you find the right home.

For detailed rate analysis, see our 2026 mortgage pre-approval guide.

Will Ventura County home prices fall in 2026?

Broad forecasts point to modest movement overall. In practice, Ventura County is many micro-markets: some neighborhoods may soften while others hold firm based on schools, commute, condition, and inventory.

If you want a precise read for your area, a comp-based snapshot is more reliable than countywide headlines.

Is 2026 a good time to buy in Southern California?

For prepared buyers, a steadier market can be an opportunity: less frenzy, more negotiation, and more time to evaluate.

Align payment comfort with neighborhood quality, and use tools like

affordability planning

to stay grounded when inventory is tight.

The advantage in 2026: unlike 2021, you’re less likely to face 10–20 competing offers on every listing—giving you time for proper due diligence, repair negotiations, and insurance verification before removing contingencies.

Is 2026 a good time to sell in Ventura County or LA?

Yes—if you price correctly and present the home well. In a market without runaway demand, execution matters more than ever:

photos, condition, pricing discipline, and a strong first-week launch.

What matters most: rates or inventory?

Both, but inventory shapes leverage. When buyers have choices, pricing discipline and condition become decisive.

When supply is tight, even small rate improvements can increase competition quickly.

What should first-time buyers focus on in 2026?

Payment planning, down payment options, and insurance diligence. Start with our comprehensive

Ventura County first-time homebuyer guide,

then narrow to neighborhoods that fit your monthly comfort zone and commute needs.

Critical 2026 tip: factor in the full monthly payment (mortgage + taxes + insurance + HOA) from day one.

Many first-time buyers in 2025 were surprised by insurance costs—don’t let that derail your offer strategy.

Use our payment calculator above to model scenarios before falling in love with a property.

How do I get a neighborhood-specific forecast?

Request a short neighborhood snapshot: current comps, buyer demand, days-on-market trend, and a pricing/offer strategy aligned with your timeline and goals.

This is the most reliable way to translate “countywide” trends into your street-level reality.

Your 2026 Southern California housing market game plan

This 2026 Southern California housing market forecast points to a more balanced, strategic market for both Ventura County and Los Angeles.

With mortgage rates stabilizing in the low-6% range and modest price appreciation expected, success in 2026 comes down to preparation over prediction.

Whether you’re buying or selling, fundamentals matter more than ever: accurate pricing, financial readiness, and understanding your local micro-market.

The neighborhoods that thrive tend to be those with strong daily-life fundamentals—schools, commute convenience, lower insurance friction, and tight turnkey supply.

Forecast references used in this analysis include: C.A.R. 2026 California Housing Market Forecast, Redfin 2026 housing predictions, Zillow 2026 housing outlook,

Realtor.com 2026 forecast reporting, and a Reuters poll on 2026 rates/prices. Local baseline metrics reference the most recent monthly trends available at time of writing.

Mortgage rate historical data sourced from Federal Reserve Economic Data (FRED), Federal Reserve Bank of St. Louis.

Ventura County Mortgage Update “` Ventura County Mortgage Rates: What the Fed’s July 2026 Decision Means for Buyers A practical look at current rates, real Ventura County payment examples, and the smartest moves buyers can make in a higher-for-longer market. Late July 2026 Buyer Financing Guide “` Ventura County Mortgage Rates: July 2026 If you have been watching Ventura County mortgage rates this month, you already know the story has not been an easy one for buyers. Rates have been climbing toward their highest levels in about a year, and all eyes turned to the Federal Reserve’s two-day meeting on July 28–29, 2026. As a local REALTOR® here in Ventura County, I get this question almost daily right now: is the Fed finally going to bring rates down? Below, I will walk you through exactly where Ventura County mortgage rates stand, what the Fed actually did, and — most importantly — what it all means for your monthly payment and your buying strategy. At a Glance What Ventura County buyers need to know “` 6.58% Average national 30-year fixed rate cited for late July $700,000 Loan amount used in the payment examples below $233/mo. Payment difference between a 6.5% and 7.0% rate “` Current Rate Environment Where Ventura County Mortgage Rates Stand Right Now “` Let’s start with the numbers, because context matters. As of late July 2026, the average 30-year fixed rate sat around 6.58% nationally, according to Freddie Mac’s weekly survey, with several daily trackers reporting rates in the 6.6% to 6.8% range. The 15-year fixed averaged just under 6%. These are national averages, however, and your actual rate in Ventura County will depend on your credit score, down payment, loan type, and the specific lender you choose. Additionally, it is worth remembering how we got here. Rates have risen steadily over the past year, driven largely by stubborn inflation, higher Treasury yields, and rising oil prices. In fact, global conflict has pushed rates higher throughout 2026, adding to the inflation pressure the Fed has been fighting. As a result, Ventura County mortgage rates today are meaningfully higher than many buyers hoped they would be by this point in the year. Keep the increase in perspective: A year ago, the 30-year fixed averaged 6.74%, so today’s rates are actually slightly lower than they were last summer and remain fairly steady compared to last month. The picture is not one of runaway increases — it is one of rates holding stubbornly in the mid-6% range while everyone waits for relief. “` Federal Reserve Decision What the Fed Decided at Its July 2026 Meeting “` The Federal Open Market Committee met on July 28–29, 2026, and announced its decision on Wednesday, July 29 at 2:00 PM Eastern Time. Heading into the meeting, markets overwhelmingly expected the Fed to hold the federal funds rate steady at its current target range of 3.50% to 3.75% — a level unchanged since December 2025. 📌 UPDATE — JULY 29, 2026 [Zac — replace this text with the confirmed outcome after 2:00 PM ET Wednesday.] Example: “As expected, the Fed held rates at 3.50%–3.75% in a unanimous vote.” Why was a hold so widely expected? Because at its June meeting, the Fed turned notably more hawkish. Officials’ updated projections showed a median expectation that rates would end 2026 higher than they are today, and most policymakers judged that inflation risks were tilted to the upside, with inflation running around 4.2%. In other words, the Fed has shifted from talking about cuts to signaling that a hike is on the table before year-end. Consequently, the July meeting was never likely to deliver the rate relief that Ventura County home buyers have been hoping for. “` Important Distinction Why the Fed Rate and Your Mortgage Rate Aren’t the Same Thing “` Here is the single most important thing to understand, and it surprises a lot of buyers: the Fed does not directly set mortgage rates. The federal funds rate is a short-term, overnight rate that banks charge each other. Your 30-year mortgage rate, by contrast, is a long-term rate that tracks much more closely with the 10-year Treasury yield and the bond market’s expectations for inflation. Therefore, even when the Fed holds its rate steady, mortgage rates can still move up or down based on what the bond market expects next. For example, if investors believe inflation will stay hot, they demand higher yields, and mortgage rates drift up regardless of what the Fed announces. On the other hand, a surprise cooling in inflation data could pull rates lower even without any Fed action at all. This is why you sometimes see mortgage rates rise on the same day the Fed holds or even cuts. The market had already priced in the decision, and it is reacting instead to the Fed’s tone about the future. As a result, the smartest move is to watch the trend in Treasury yields and inflation reports, not just the headline Fed decision. The practical takeaway A Fed announcement can influence mortgage rates, but it does not mechanically determine the rate a Ventura County buyer receives. “` Real Payment Examples What Today’s Rates Mean for a Ventura County Home Payment “` Numbers on a screen are abstract, so let’s make this real for a Ventura County buyer. Because our county’s home values run well above the national average — many cities sit comfortably in the mid-$800,000s — even small rate changes move your payment significantly. Consider a $700,000 loan, roughly corresponding to a home in the mid-$800,000s with 15% to 20% down. Here is how the estimated principal-and-interest payment shifts across a realistic rate range: 30-YEAR RATE EST. MONTHLY P&I CHANGE FROM 6.5% 6.50% About $4,424 Baseline 6.75% About $4,540 About $116 more per month 7.00% About $4,657 About $233 more per month Illustrative principal-and-interest estimates only. Property taxes, homeowners insurance, mortgage insurance, HOA dues, lender fees, and other housing expenses are not included. Monthly impact About $233 Annual impact Nearly

Median Home Price in Moorpark, CA (2026) Moorpark Housing Market 2026 Median Home Price in Moorpark, CA (2026): What Real MLS Data Shows A local, data-backed look at Moorpark home prices, year-over-year trends, days on market, and what buyers and sellers should know right now. Overall Median $980,000 Single-Family $1.035M Median DOM 35 Days Quick Answer The median home price in Moorpark, CA in 2026 is approximately $980,000 across all residential property types. The median single-family home is approximately $1,035,000, while condos and townhomes remain more accessible at medians of $528,000 and $615,000. If you have been searching for the median home price in Moorpark, CA in 2026, you have probably found a confusing mix of estimates from national websites that rarely agree with one another. So I did something different. I pulled the actual closed-sale data from our local MLS — every recorded Moorpark sale over the past two years — and ran the numbers myself. As a result, what follows is not a guess or a national algorithm’s best approximation. It is the real story of what homes in Moorpark are actually selling for right now. The short version: Moorpark has been remarkably steady. The median home price in Moorpark for 2026 sits right around $980,000 across all property types, essentially flat compared with a year ago. However, that headline number hides some important detail, especially if you own a single-family home. Let’s walk through exactly what the data shows. Current Market Snapshot Median Home Price in Moorpark, CA: The 2026 Snapshot Over the trailing twelve months, nearly 300 homes closed escrow in Moorpark (zip code 93021). Based on those verified MLS sales, here is the current picture: All Residential $980,000 Median sale price Single-Family $1,035,000 Median detached home Condominium $528,000 Median condo price Townhome $615,000 Median townhome price Price Per Sq. Ft. $447 Median price per square foot Market Time 35 Days Median days on market Therefore, when someone asks what the “typical” Moorpark home costs, the most accurate answer is around $980,000 across everything — but a standard single-family house now runs comfortably north of a million dollars. That gap matters, and I will explain why in the next section. Property-Type Comparison Single-Family, Condo & Townhome Prices: A Breakdown The all-property median can be misleading because Moorpark’s market is really three markets stacked together. Single-family homes make up roughly 80% of local sales, while condos and townhomes make up the rest. As a result, the blended $980,000 median lands below the single-family figure, because the more affordable attached homes pull the overall number down. Property Type Median Price What It Means Single-Family Homes $1,035,000 The segment most relevant to the majority of Moorpark homeowners. Townhomes $615,000 A more attainable ownership option without a seven-figure price tag. Condominiums $528,000 The most accessible entry point into the Moorpark market. Single-family homes carry a median of about $1,035,000. This is the number most Moorpark homeowners actually care about, since the vast majority of the city’s housing is detached single-family. Townhomes sit at a median of $615,000, offering a meaningful entry point for buyers who want to own in Moorpark’s excellent school district without a seven-figure price tag. Condominiums are the most accessible option at a $528,000 median. Consequently, if you are a first-time buyer, the condo and townhome segments are where Moorpark opens up. Additionally, if you are comparing Moorpark to nearby cities, it helps to look at the Simi Valley median home price right next door, as well as the broader median home price across Ventura County for context. Year-Over-Year Movement How Moorpark Home Prices Changed Year Over Year This is where the data gets genuinely interesting. Despite plenty of national headlines about prices climbing or falling, Moorpark has mostly held its ground — with a slight cooling underneath the surface. Comparing the most recent twelve months against the prior twelve months: Overall Median 0.0% Held flat at $980,000 Single-Family Median -2.8% $1.065M to $1.035M Price Per Sq. Ft. -4.0% $466 to $447 In other words, Moorpark did not crash, and it did not surge. Instead, prices have plateaued, with a gentle downward drift in the single-family segment. This kind of flat-to-slightly-soft pattern is exactly what we have been seeing across the region, consistent with the statewide trends tracked by the California Association of REALTORS®. For the bigger picture, our latest Ventura County market update shows the same theme playing out county-wide: stability, not fireworks. Budget Breakdown What About $1 Million Buys in Moorpark Right Now Since the single-family median lands just over a million dollars, it is worth breaking down what your budget actually gets you. Using this past year’s closed single-family sales, here is the median by bedroom count: 3 Bedrooms $835,000 4 Bedrooms $1,075,000 5 Bedrooms $1,428,000 So the classic four-bedroom Moorpark family home is the heart of the market, and roughly a million dollars is the going rate. Meanwhile, smaller three-bedroom homes remain the most attainable path into single-family ownership, and larger five-bedroom properties command a clear premium. For reference, single-family sales this year ranged from around $435,000 on the low end all the way up to $5.5 million for Moorpark’s most exclusive estates. Market Leverage Days on Market & Sale-to-List: How Fast Are Homes Selling? Price is only half the story. How quickly homes sell, and how close they get to asking price, tells you who holds the leverage. Here is what the Moorpark data shows for 2026: Median Market Time 35 Days Up from 33 days Sale-to-List 99.4% Of final list price Over Asking 28% Of closed sales Under Asking 55% Of closed sales Where Moorpark homes closed versus asking price 28% over asking 17% at asking 55% under asking Therefore, the typical Moorpark seller is still getting very close to their asking price — but the days of automatic bidding wars are behind us. Because most homes now close slightly under list and take a bit longer to sell, buyers have regained a measure of negotiating room they simply did

Can ChatGPT sell your house in 2026? Here’s what AI does well, where it falls short, and what it can cost Ventura County sellers in a softening market.

Oxnard’s median home price is $785,000 in 2026, but prices vary sharply by zip code, property type, and neighborhood. See real MLS closed-sales data, current market trends, and what the numbers mean for Oxnard buyers and sellers.

Oxnard’s median home price is $785,000 in 2026, but prices vary significantly by zip code and property type. Explore real MLS closed-sales data, current market trends, and what today’s numbers mean for Oxnard buyers and sellers.